On the performance of Bitpanda Crypto Index

Bitpanda is an established fintech company based in Austria providing cryptocurrency and blockchain oriented services to customers from all over the world with primary focus on the European market. Bitpanda was founded in 2014 as a crypto broker and added crypto exchange to its portfolio in late 2019. Recently, Bitpanda has come up with another brand new product that further reinforces its position in the crypto landscape, namely crypto indices, which will be subject of this memo.

Bitpanda Crypto Index, or BCI, is pretty much what its name suggests — a standard financial index product measuring performance of selected crypto currencies based on predetermined allocation criteria. Cornerstone of BCI (and of indices in general) is to maintain a diverse portfolio of assets such that portfolio value is on par with average market performance or ideally outperforming it. While these two goals (diversification and performance) are common for all (crypto) indices, their particular implementation is what sets index apart from the competition and what will ultimately attract customers.

In the following paragraphs I will try to present how BCI puts above attributes into practice and how it is doing when compared to alternative approaches with primary focus being put on the analysis of portfolio value and its evolution over the time.

Before we delve into the performance analysis of BCI let me very briefly summarize its methodology (for full product description see the prospectus). BCI allocates selected number of crypto currencies (5 assets in case of BCI5 product, 10 in case of BCI10 or 25 in case of BCI25) which are subject to regular rebalancing aiming to reflect shifts in the market. Rebalancing takes places once a month and redistributes portfolio according to the following rules (BCI5 is used for illustration):

- first build a list of new index candidates: (1) include all currencies from the current index with average daily traded value (volume*price) over past 30 days ≥ $600,000 (2) include remaining currencies ordered by market capitalization with average daily traded value over past 30 days ≥ $1,000,000 until the list contains 10 currencies

- take top three currencies according to their market capitalization from the candidate list and definitely add them into the new index portfolio

- put additional two currencies from the candidate list into the final index such that currencies from the existing index ranked up to the 7th place according to the market capitalization take priority

- build and normalize currency weights according to their market capitalization

- cap allocation to 35% and renormalize (the step can be performed multiple times)

Having described BCI’s rebalancing rules we can now look how they impact BCI composition and consequently the portfolio value and benchmark them with other strategies. For sake of this report I chose two competing strategies where the first one (denoted by TopX) always allocates top X currencies according to their market capitalization and employs regular rebalancing, and the second one (denoted by HODL) which allocates top X currencies and HODLs them until the end of time. Each execution starts with $1000 and applies 2% rebalancing fees for buying and selling the currencies. Simulation ran over various time frames, the oldest one dating back as long as 2015. Each time period ends 01/11/2020. The comparison focuses only on BCI5 and BCI10 indices because BCI25 involves slightly different rebalancing rules which were not implemented. In all strategies the maximum asset allocation is restricted to 35% (in case of 5 assets) or 30% (in case of 10 assets) to achieve desired diversification. Even though I tried to follow bitpanda rebalancing rules as much as possible, it is possible that actual update of portfolio performed by bitpanda might slightly differ, mainly due to certain steps not being explicitly disclosed and bitpanda reserving rights to adjust the rules fully at their sole discretion. Nevertheless, outcome of the simulation still provides valuable insight into mechanics of the index and its evolution over time.

So much for description, let us look at hard data and analyze them from various angles (complete figures can be viewed via Google Sheets):

First of all it immediately follows that regardless of the strategy used it was almost always beneficial to invest into crypto currencies. Except if one entered crypto market at the beginning of 2018 when currencies were reaching their ATH the returns were always positive and sometimes even by several orders of magnitude. This alone is satisfying though not so surprising.

What is more interesting is the pair-wise comparison of the strategies. If we consider solely the average gains, then the clear winner is BCI with average gain of 2469% in contrast to TopX with 1610% and HODL with 2074%. This is a good indication that BCI rebalancing rules are solid and outperform both average market gain as well as leading currencies. From these numbers it is also visible that a strategy as simple and straightforward as HODLing may actually outperform more sophisticated strategies employing more complex algorithms. At first sight this need not be obvious and we might even say it is surprising as one could expect that sticking to the most performing currencies (according to the market capitalization) would certainly pave the way to a maximized portfolio. We can attribute this phenomenon to not-so-rare turbulent rearranging of leading crypto currencies and consequently realizing a potential loss when currencies are kicked out of the index (in which case entire position of the currency is sold and replaced by another one). Although BCI takes the lead when average gains are concerned we may notice that it is due to substantial profits of positions entered during the bull market (2015–2018) which outweigh losses if entered in the subsequent corrective period (2018–2020). In this latter period we would have been again better off simply sticking to HODL strategy. Maybe it is Occam’s razzor kicking in. It is worthwhile to mention that evolution of the portfolio over the time is quite sensitive to the initial portfolio distribution and its rebalancing parameters. For instance, capping maximal allocation of assets in TopX strategy from 35% to 80% (hence decreasing diversification) decreases final portfolio value by 500 percentage points. Another evidence that diversification of the portfolio does actually improve the performance.

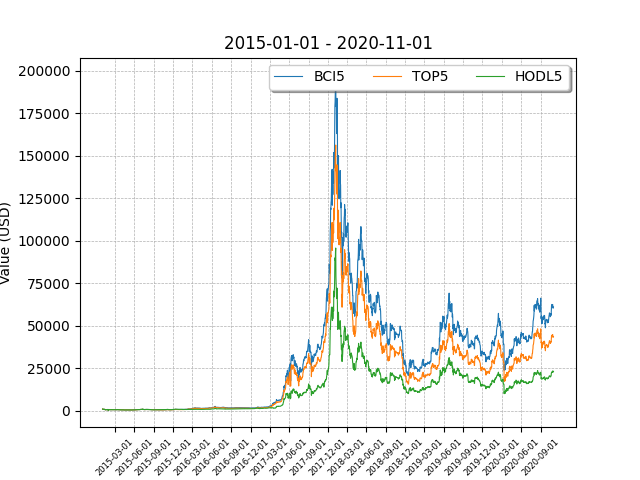

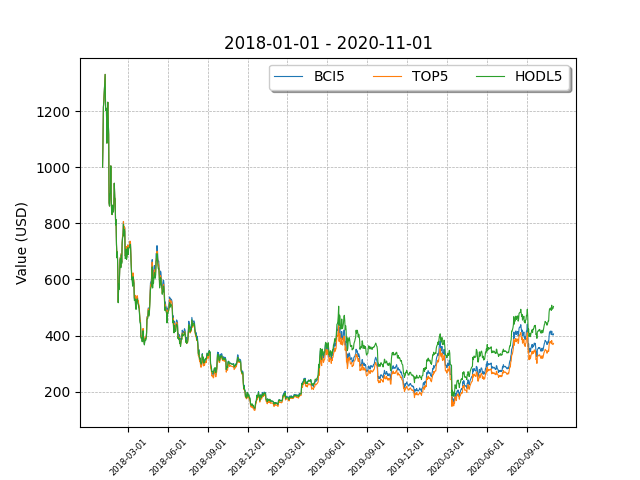

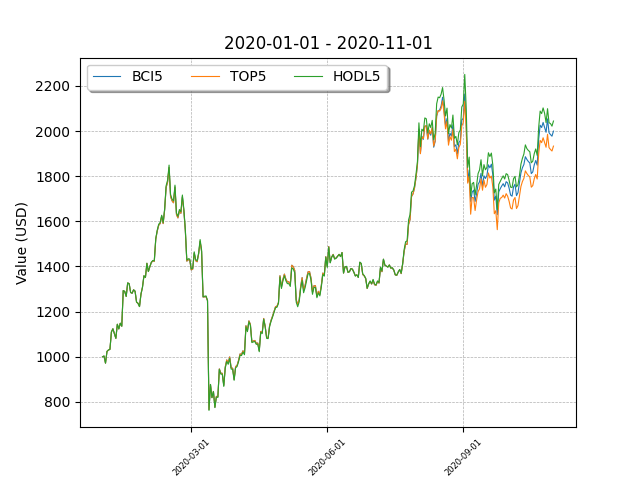

Besides comparing final portfolio value it is also interesting to see how the portfolio was doing during the period in between. Below you can find three graphs for periods starting in 2015, 2018 and 2020. What is striking is that BCI would yield ~20,000% profits at a certain point compared to ~15,000% profit of TopX and ~10,000% profit of HODLing. Not bad.

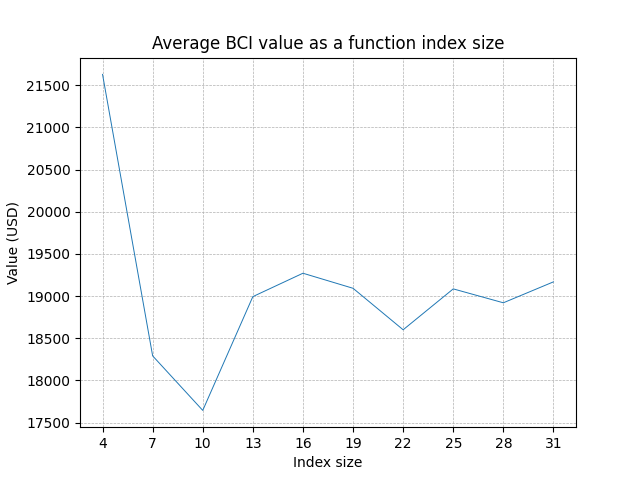

Next I would like to talk about different variations of BCI. As previously mentioned there are currently three variants of BCI differing primarily by number of assets in the portfolio and then by configuration of certain parameters, such as maximum allocation, preference of assets already included in the index and others. While higher number of assets naturally helps diversification in vast majority of simulations indices with higher number of constituents were on average underperforming compared to their ‘lighter’ counterparts, though the value stabilized once reached a limit, see below. This is explained by asymmetric distribution of market capitalization which follows fat tail distribution and simultaneous capping of the top performing currencies.

So how was BCI doing when confronted with historical data and other strategies? I would say quite well. In the bull market it gave better than average results and in some cases even extraordinary ones. During the bear market it slightly underperformed but still within reasonable bounds. If history repeats and one exits position at the right time, he or she can end up with significant gains. As far as diversification is concerned, the immediate returns go against it as illustrated in the figure above. As a matter of fact, BCI10 gave the worst performance out of all index sizes. Last but not least, one should not neglect fees paid for the rebalancing. Current bitpanda’s 2% fee is pretty high (but it is in line with other fees on the broker’s platform and you pay for the service) and it can eat non-trivial portion of the profits easily. For instance, during the bull market fees climbed as high as $6,468, though the net gain still achieved good results. It might discourage some people nevertheless and they may decide to do rebalancing themselves on an exchange manually.

By now I have been presenting nothing but facts based on historical simulations and I would like to conclude with a few personal views. Given current and past crypto market conditions I am not 100% convinced about investing into crypto indices right now if ones seeks the same financial product as offered by ‘standard’ markets. At the moment I still view them as a means of speculation akin to other crypto trading strategies. This by no means disqualifies BCI (or crypto indices in general), I am just saying their utility function might be currently different than what we see in other markets. This does not have to do so much with the methodology of the indices as such but more with the underlying crypto currencies which constitute the indices. They bear all the pros and cons we have been witnessing over the past couple of years. But it is not as pessimistic as it might sound, I am strongly convinced the opposite is true. All simulations were based on historical data dating between 2015 and 2020. During that time crypto currencies and related crypto landscape were still in their infancy and were attracting a lot of speculators and frauds. Today situation is significantly different. Unlike somewhat irrational crypto booms from the past the wheat has been separated from the chaff and crypto technologies advanced by a huge extent. They are no longer projects with a roadmap into next three, five or ten years (or a plain scam) but they are effectively penetrating into regular real business as we are speaking (it goes without saying there is still a plenty of shady parts of the crypto space). Crypto indices and BCI will definitely leverage this and I am sure they will solidify their position, though it may still require a little bit more time.

All experiments described in the article were simulated with bci-simulator which is a Python package available in GitHub and you can use it to conduct your own simulations. More info is available on the project page.

I am not affiliated with bitpanda, though I have been their customer for a couple of years. If you want to support development of other crypto libraries, tools and analyses, then it will be of great help if you donate an arbitrary tip:

- BTC:

3GJPT6H6WeuTWR2KwDSEN5qyJq95LEErzf - ETH:

0xC7d8673Ee1B01f6F10e40aA416a1b0A746eaBe68